Time Weighted Rate of Return: Measuring True Performance

When evaluating investment performance, there's a fundamental problem: External cash flows distort the results. When you deposit or withdraw money from your portfolio mid-year, traditional return calculations become misleading.

The Time Weighted Rate of Return (TWRR) elegantly solves this problem and is therefore the gold standard for performance measurement in the financial industry.

The Problem: Cash Flows Distort Performance

Imagine you have a portfolio worth $10,000. After 6 months, it's worth $11,000 (+10%). Then you invest another $10,000. After a full year, your portfolio is worth $22,000.

Wrong calculation: "I invested $20,000 and now have $22,000, so that's +10% return."

The problem: The second $10,000 only had 6 months to work, not 12 months. The calculation mixes investment performance with cash flow timing.

The Solution: Time Weighted Rate of Return

TWRR eliminates the influence of inflows and outflows by measuring performance over individual periods between cash flows and then linking them together.

Basic Principle

- Split periods: Each cash flow (deposit or withdrawal) marks the end of a measurement period

- Calculate individual returns: Measure pure investment performance for each period

- Chain returns: Individual returns are linked multiplicatively

Formula

For n periods between cash flows:

TWRR = (1 + R₁) × (1 + R₂) × ... × (1 + Rₙ) - 1

Where R₁, R₂, ..., Rₙ are the returns of individual periods.

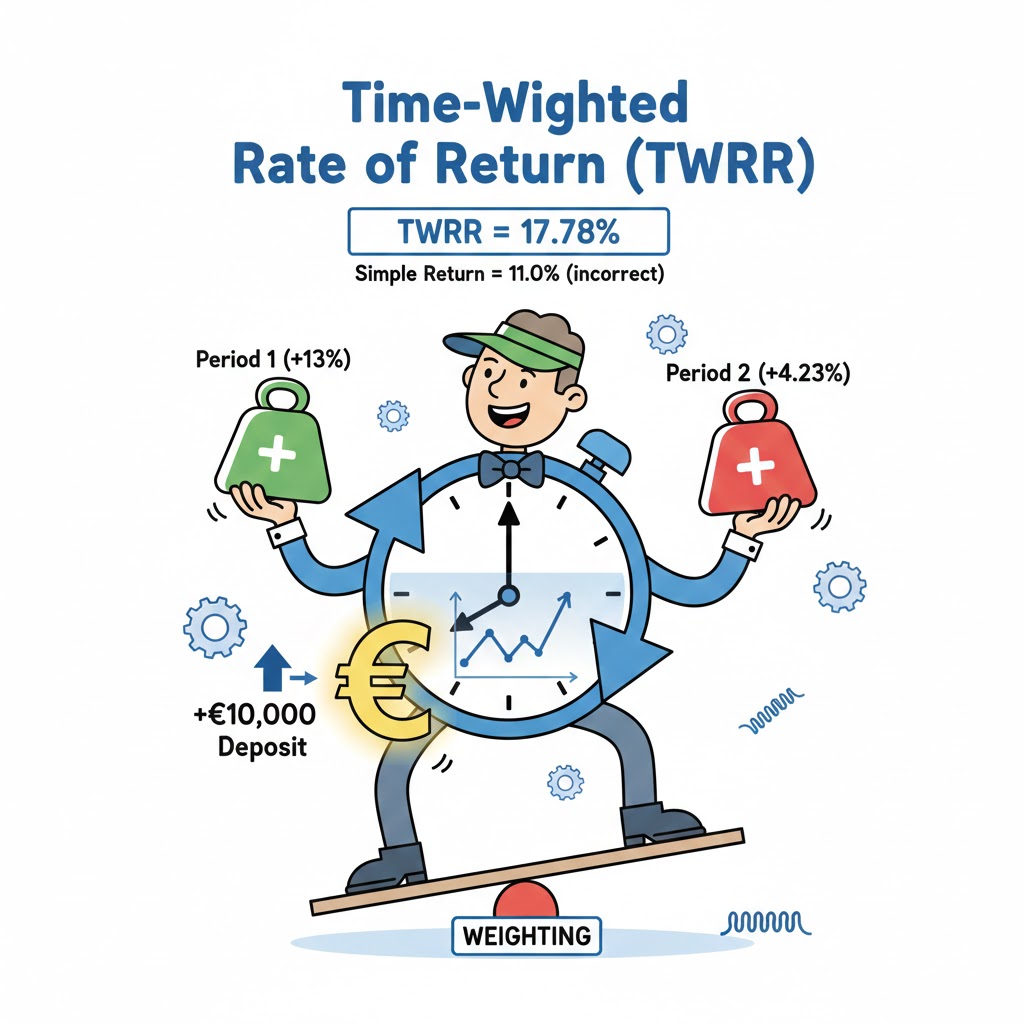

Interactive Example: TWRR vs. Simple Return

TWRR vs. Money Weighted Return (MWR)

While TWRR measures pure investment performance, the Money Weighted Return (MWR) considers the timing of cash flows.

| Metric | Purpose | When to use? |

|---|---|---|

| TWRR | Pure performance measurement | Fund comparison, manager evaluation |

| MWR | Investor-specific return | Personal success calculation |

Example of the Difference

Scenario: A fund rises 20% for 6 months, then prices fall. An investor adds money exactly at the peak.

- TWRR: Shows the actual fund performance (+20% then -X%)

- MWR: Shows the investor's poor return (due to bad timing)

Practical Application

1. Fund Manager Evaluation

TWRR is the standard for evaluating fund managers because it separates their skill from cash flow timing.

2. Benchmark Comparisons

Only with TWRR can you fairly compare: "Did my portfolio outperform the S&P 500?"

3. Portfolio Optimization

TWRR helps identify which strategies work, independent of timing of your deposits/withdrawals.

Calculation in Practice

Step-by-Step Guide

- Identify all cash flows (deposits and withdrawals) with dates

- Split the time period into periods between cash flows

- Calculate for each period: R = (End value - Cash flow) ÷ Beginning value - 1

- Chain the returns: TWRR = (1 + R₁) × (1 + R₂) × ... - 1

Simplification with Frequent Cash Flows

With monthly savings plans, a modified Dietz method is often used, which provides a good approximation to TWRR but is easier to calculate.

Conclusion: Why TWRR is Indispensable

-

Objective performance measurement: TWRR shows true investment performance, independent of cash flow timing

-

Comparability: Only with TWRR can you fairly compare different investments

-

Manager evaluation: TWRR separates investment skill from investor timing

-

Industry standard: All professional performance reports use TWRR

The Time Weighted Rate of Return is the most precise tool for measuring investment performance. Without it, you're flying blind in portfolio analysis.

💡 Tip: Use totallynotrich.com for TWRR calculations in your backtests and portfolio analyses. All simulations automatically use time-weighted returns for accurate performance measurement.